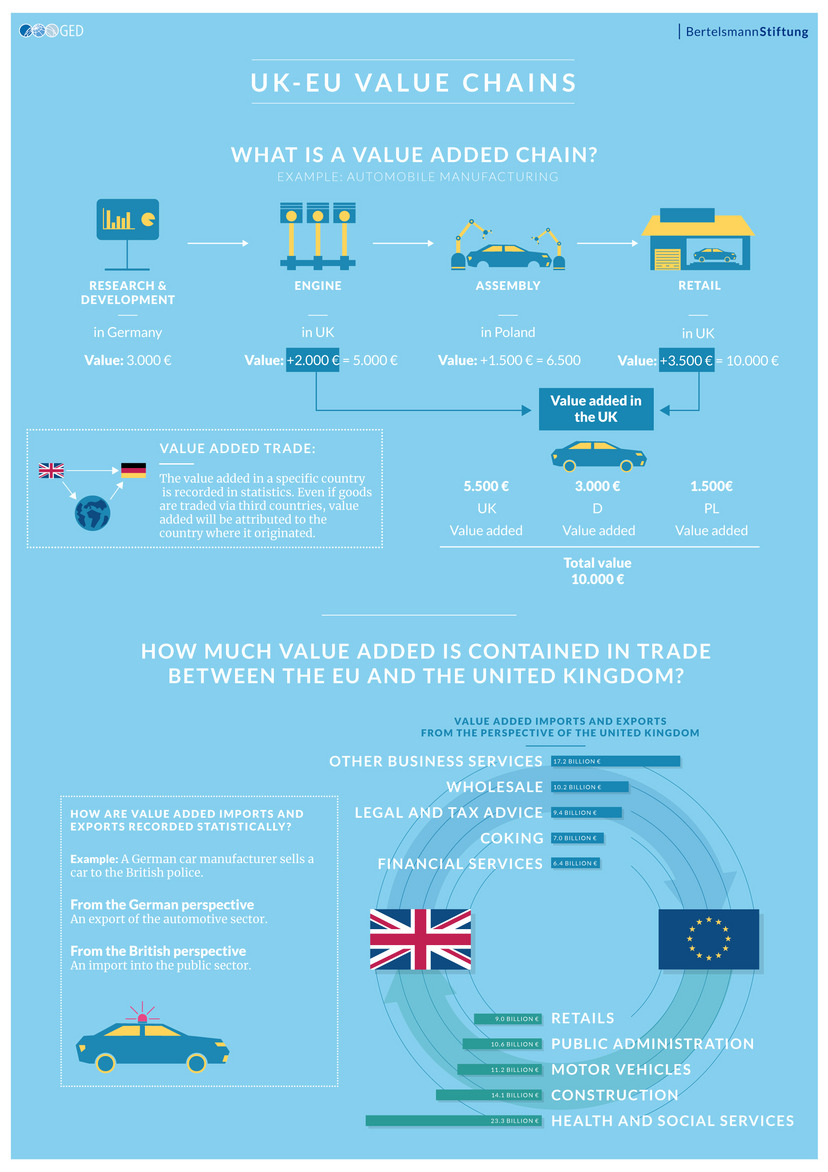

For the UK, Germany is the second most important export market (after the USA), while the UK is the fourth most important export market for Germany. Germany buys goods and services worth 115 billion euros from Great Britain, whereas Great Britain still buys 70 billion goods and services from Germany. Brexit inevitably leads to an increase in trade costs. A new study examines to what extent value chains between the two countries are exposed to this increase.

Value-added is the additional value that an additional production step adds to an intermediate product. Import and export statistics show how much value-added was created along a production chain in each participating country. On this basis, this study examines how much British value-added is processed in German industries and, conversely, how much German and European value-added is processed in British industries. Since trade costs will rise as a result of Brexit, there is a need for adjustment in the German sectors which are particularly closely linked to Great Britain and vice versa – either by passing on the higher production prices or by shifting production steps away from Great Britain. For example, if a German car manufacturer is currently importing a part from the UK to be used in its cars worth 100 Euros, tariffs will increase that price to 110 Euros. That might make it worthwhile for the manufacturer to source that part elsewhere, say Poland, where there is a manufacturer that makes the same for 105 Euros. In this example, the British producer and the consumer loses as the part is no longer made in the cheapest available place.

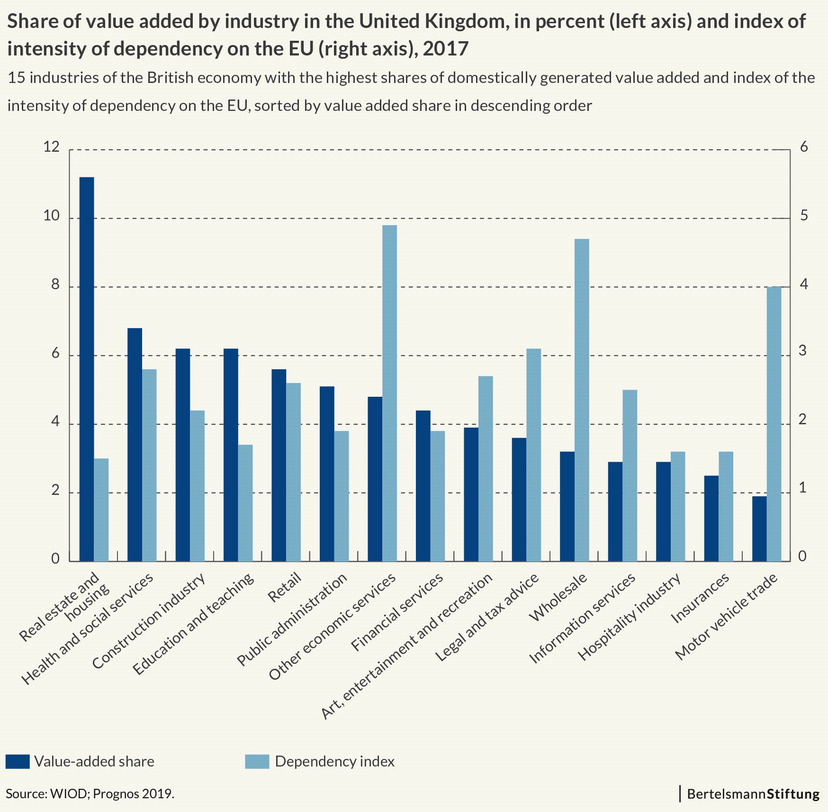

For Germany, the study shows that there is a considerable need for adjustment in individual sectors, but this tends to be in sectors that account for a smaller share of the total value-added of the German economy (see graph).